Serving clients on every continent, routinely named one of the top five law firms in the U.S. for its hedge fund practice, and frequently honored for outstanding results, Sadis is known nationally and internationally as a dominant force in the financial services sector.

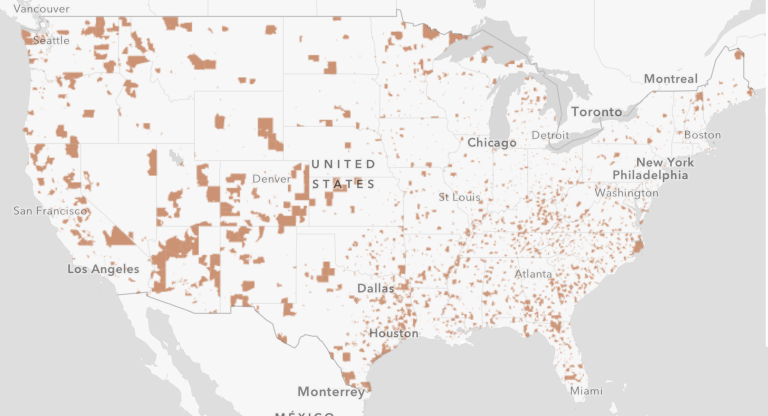

The 2017 tax reform legislation, the Tax Cuts and Jobs Act (“TCJA”), has created a significant new income tax incentive for taxpayers to make investments in designated low-income areas, known as Qualified Opportunity Zones (“QOZ”). The new tax provisions (Internal Revenue Code Sections 1400Z-1 and 1400Z-2) provide for a deferral of capital gains realized on sales of “any property” to an unrelated party where an amount equal to such gain is reinvested in a Qualified Opportunity Fund (“QO Fund”) within 180 days, as well as other substantial tax preferences, as discussed below. In addition, certain amounts of the capital gains tax attributable to the reinvested money may be permanently exempted from tax if the investment in the QO Fund is held for longer than 5 or 7 years (10% and 15%, respectively), and if the investment in the QO Fund is held for at least 10 years, any gain from post-investment appreciation in the QO Fund is permanently excluded from tax.

With decades of experience in structuring private fund vehicles and experts in fund structuring, real estate and international taxation, the opportunity zone team at Sadis stands ready to guide you through any concerns relating to structuring a fund, executing a QOZ investment strategy, and handling any tax and commercial considerations.

For more information regarding opportunity funds, reach out to one of our practice contacts.